Income protection insurance through superannuation vs direct

Explore the differences between income protection insurance through superannuation or direct insurance....

To make sure you receive the highest standard of service when taking out cover, we comply with the Life Insurance Code of Practice. Read more

When choosing the amount of cover you want to be insured for, you should consider things such as your monthly debt repayments (mortgage, personal loans or credit cards) and weekly expenses (groceries, utilities, out of pocket school costs) to make sure you have enough to cover all outgoing expenses until you are back at work.

With Real Income Protection Insurance, you can get cover up to 70% of your pre-tax income as a monthly benefit up to $15,000 per month – but what does this mean for you?

The following table breaks down salary ranges and the potential monthly benefit based on that salary:

| Annual pre-tax salary | Monthly pre-tax salary | Potential monthly benefit |

|---|---|---|

| $100,000 | $8,333 | $5,833* |

| $75,000 | $6,250 | $4,375* |

| $50,000 | $4,167 | $2,917* |

*Your potential monthly benefit payable may be different to the monthly amount insured as it will be reduced if you are receiving other disability payments e.g. workers compensation or sick leave and will depend on your income at the time of claim. | ||

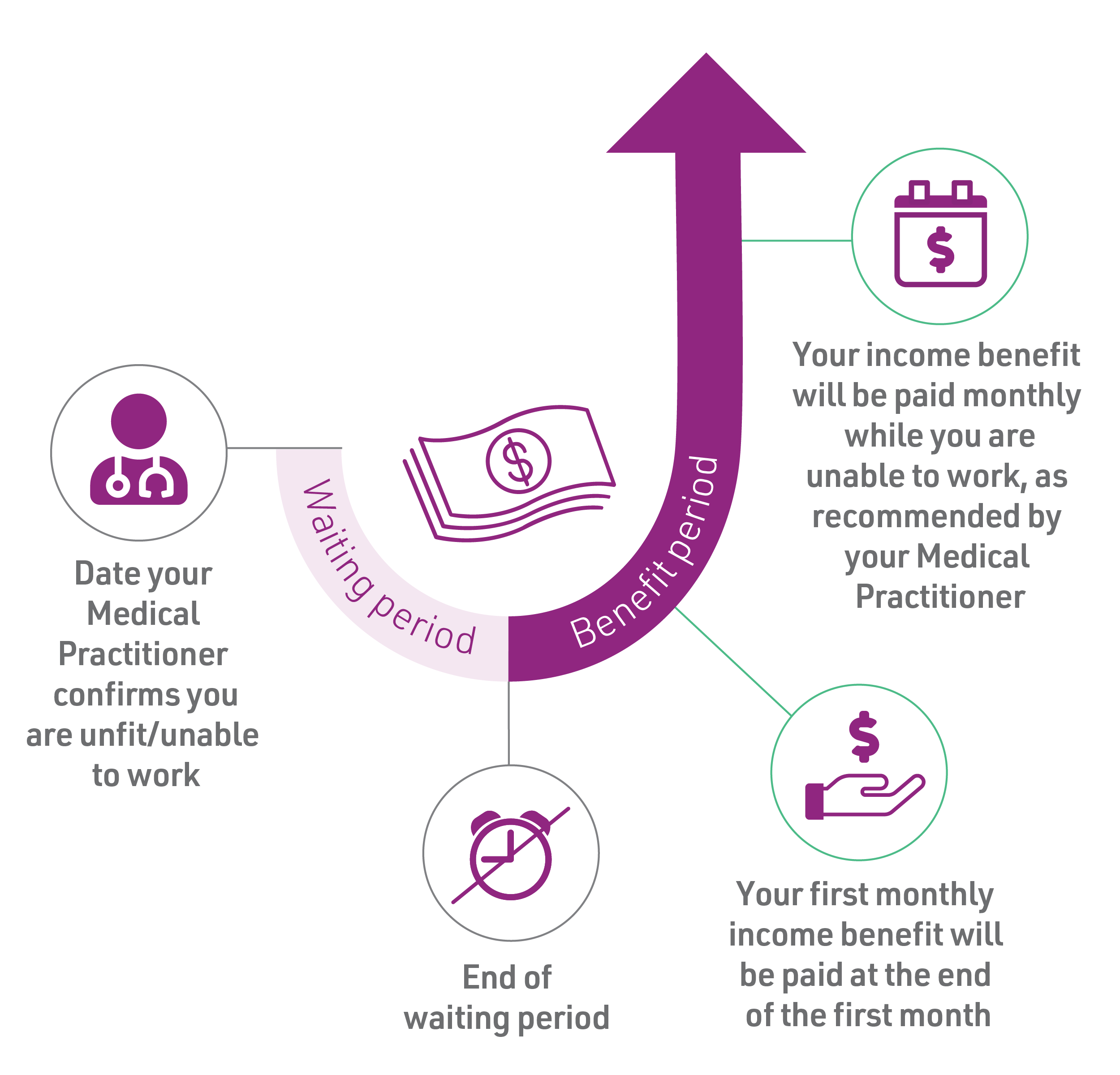

The waiting period is the time you have to wait before your income benefit payments are payable and will affect the cost of your monthly premiums. When applying for your policy, you can choose a waiting period of 30 or 90 days.

At Real Insurance we pride ourselves on providing trusted service and real value to our customers, which has been recognised by 16 consecutive years of industry awards.

Everyone’s individual situation differs. Some of the things to consider when choosing whether to purchase cover can include:

If you are self-employed and don’t have access to sick-leave and paid time off, income protection insurance could provide financial security if you are unable to work due to injury or sickness. If you have dependents, income protection insurance could help make sure they are financially secure if you are unable to work.

If you have financial commitments, such as a mortgage, income protection insurance could help you continue to make repayments even if you are unable to work.

Income protection insurance could also be beneficial if you don’t have enough savings to cover your expenses while you are off work and not earning any income for several months or more.

If you are unsure whether you need income protection insurance, speak to your financial advisor.

If you are unable to work due to an injury or sickness, Real Income Protection Insurance covers up to 70% of your pre-tax income up to $15,000 a month, so you can focus on getting back on your feet without added financial stress.

As well as helping you cover everyday living expenses and pay mortgage or credit card repayments on time, in addition you could be reimbursed for some of your rehabilitation program or return to work costs. You could modify your house to make it more accommodating for your new circumstances, or your loved ones could receive a final expenses benefit to help them cover your funeral expenses if the worst happens while your cover is active.

Learn more about what income protection insurance covers.

Yes, according to the Australian Tax Office (ATO) you may be able claim the cost of your income protection insurance premiums against any loss of income. When considering the tax implications of Real Income Protection Insurance, always seek professional advice. Learn more about is income protection insurance tax deductible?

Yes, there may be some exclusions. No income benefit will be payable if the injury or sickness is caused directly or indirectly as a result of:

Other exclusions may apply. Please read the Real Income Protection Insurance PDS for further details.

Yes, your job could affect the premium you pay. With Real Income Protection Insurance, premiums are determined by several factors including the duties you perform as part of your work, as well as your age, smoking status, and more.

Claims should be made as soon as possible after the incident giving rise to the claim.

Visit our claims page for more information.

Your dedicated claims specialist will provide you with a claim form as well as details of any other documents that may be required which will include:

Visit our claims page for more information

Once we receive all the documentation we have asked for, your claim will be submitted to Hannover (insurer) to be assessed. We will call you as soon as there is an update or within 10 business days of receiving your forms, and every 10 business days thereafter to keep you informed of how your claim is going.

If your claim is approved, payment will be made promptly. Sometimes assessment leads to a need for additional information. This may require you to provide the extra information, or we may seek it directly from your medical practitioner. In either case, we will consider any new information promptly and inform you of the outcome.

You will receive a monthly payment. You can start to accrue payments once you have been unable to work for longer than 30 or 90 days, depending on the waiting period you have chosen. Payments are made at the end of the month and then will continue each month you are out of action up to 6 months, 1 year, 2 years, or 5 years depending on the benefit period you have in your policy cover.

The payments will be made directly to the bank account that you nominate on your claim form.

Explore the differences between income protection insurance through superannuation or direct insurance....

Discover income protection for sole traders. Compare policies, get tips, and consider cover to safeguard your...

Is there enough in your emergency fund? Dive into our guide to income protection insurance and explore the...

Job interviews can be stressful and intimidating. Improve your chances of having a great interview by...

Life insurance and income protection insurance cover different things? This article explains the differences...

Get clear information about income protection insurance so you can make a sound decision regarding your...

Exclusions applicable include but are not limited to, no cover for injury or sickness caused through an intentional or self-inflicted act, war or riot, engaging in criminal acts or associated with pregnancy or elective surgery. For further details please read the PDS.